What We've Learned from Surveying 300 Icelandic Entrepreneurs

Iceland's innovation ecosystem has been transformed over the past six years: business R&D surged as venture capital matured and public innovation support expanded considerably. Fresh feedback from the community reveals that the majority of Icelandic innovators remain positive about the future of innovation in the country. But this optimism coexists with a sense of persistent frictions across the ecosystem.

In the spring of 2025, Northstack and Tækniþróunarsjóður launched Nýsköpunarlandið 2.0, a follow-up to a 2019 survey that tracked how Iceland's innovation community perceived their operating environment. We surveyed nearly 300 founders, CEOs, and R&D managers who had applied for Technology Development Fund grants over the past decade to understand how their perceptions had shifted, where they diverged from objective indicators, and which issues deserved policy attention.

What emerged from the 2025 survey was a shared sense of optimism about the future, with men and women and capital and countryside innovators similarly positive about Icelandic innovation’s prospects. Yet we also noticed signs of structural challenges limiting innovative companies' ability to grow, from talent access to banking services and currency-related uncertainty. These issues are also reflected in Iceland's global innovation rankings, which have remained largely stagnant despite increased R&D spending over the same period. Together, they suggest that the barriers to successful innovation run deeper than funding alone.

Innovation policy beyond R&D support

Debates about innovation policy these days often focus on targeted instruments, from R&D tax credits and grants to state-backed VC funds. These aspects are certainly very important, and our detailed survey covers many of them. But our findings also make clear that a far broader range of factors shapes whether companies can actually innovate and grow.

From education and immigration policies to the quality of financial services and currency stability, structural dimensions operate in the background but fundamentally constrain what innovators can achieve. This echoes a broader global conversation, exemplified by this year’s Nobel Prize in economics, on how institutions determine whether technological progress translates into sustained growth. The 2025 laureates Joel Mokyr, Philippe Aghion and Peter Howitt demonstrated the crucial role of systems and institutions in turning ideas into impact. Direct innovation support, in this light, is only one piece of the puzzle. Sustainable growth depends on societies willing to embrace change, on institutions capable of overcoming resistance from established interests, and on the alignment of practical, technical, and commercial knowledge. Production, R&D, finance, and even household savings are interlinked and cannot be understood in isolation.

Our survey results illustrate this principle in practice. Just around half of respondents find access to talent good. Banking services have improved but remain middling: only one in five rate them as good. The króna continues to weigh on businesses. Respondents highlight the impact of high domestic interest rates: “Real interest rates are exceptionally high; today, business operations struggle to compete with the guaranteed returns of a savings account. The incentives for investment, particularly in high-risk ventures in innovation, have effectively been removed.” These aren't problems that additional R&D grants directly address.

Persistent frictions

Access to local talent has improved since 2019: 48% now rate it as good, up from 39% six years ago. Computer science graduate numbers have grown steadily, a genuine bright spot. But doctorate numbers have declined and science and engineering graduate shares remain low in international comparison, suggesting the local talent base is narrowing in some critical areas even as it expands in software.

For foreign talent, the picture is mixed. Actual hiring has grown in our sample, from 40% to close to 50% of surveyed organizations employing foreign specialists, yet perceptions of ease of access haven't kept pace. With upheaval in the U.S. science sector creating opportunities to attract researchers from overseas, administrative barriers should be examined and removed, argue our respondents: “There is room to streamline the application process for work permits and tax incentives for foreign experts. As it stands, these applications drag on for months; if Iceland wants to remain competitive, we need to be measuring that turnaround in hours."

Banking services represent another infrastructure gap. Overall, startups’ priorities for the banking system were pragmatic: better international payment processing, more creative financing options, and lower costs. To our surprise, several survey respondents specifically highlighted access to services like Stripe and Revolut as the main improvement they wished to see.

The Icelandic króna also remains a constraint, though less acutely than in 2019. 62% of respondents still describe its impact on business as negative, down from 74% in the previous survey. Despite a period of relative stability in 2024, favourable views remain rare and many respondents continue to associate the currency with uncertainty.

Barriers to growth

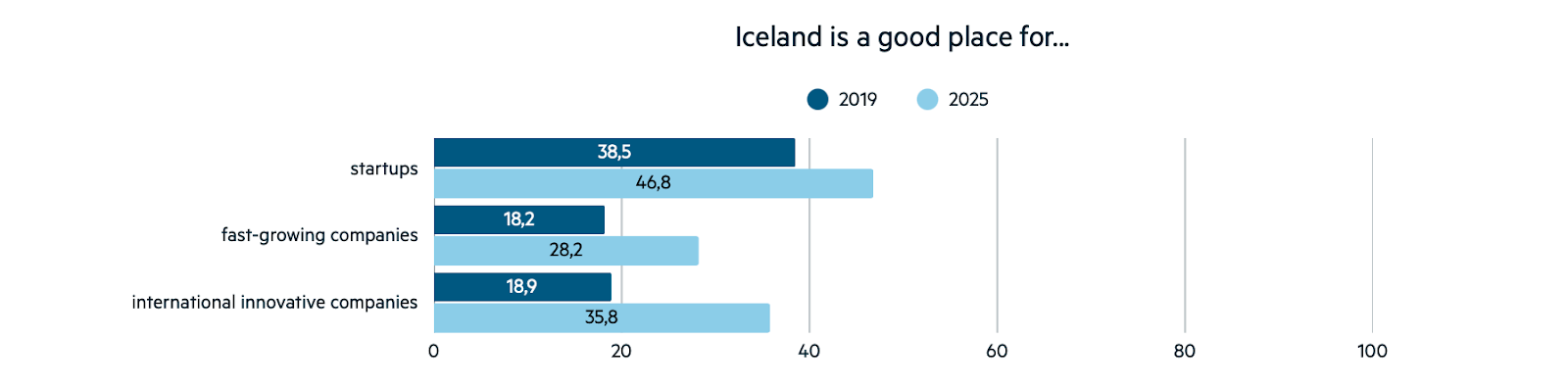

Our data show a clear pattern: innovators see Iceland as favourable for startups but challenging for scale. Nearly half of our respondents rate it attractive for early-stage ventures, while fewer than one in three consider it suitable for rapid growth.

Figure: Share of respondents who agree that Iceland is a good place for companies in different stages, 2019 vs 2025

The constraints most often selected in the survey are familiar: a small domestic market, high labor costs, high taxes. Our open-ended questions also reveal something more specific. Respondents point repeatedly to a funding gap between the grant and pre-seed stage and more sizeable Seed / Series A rounds, especially for companies who do not yet have a large revenue stream: “Few funds in Iceland make seed investments in the 50–200 million ISK range. Many venture capital funds want to see at least 100 million ISK in annual revenue before they get involved. There is simply too much risk aversion, and many promising companies and strong teams end up giving up because no one is willing to invest in them.”

Together, these responses suggest that public innovation support and investment options could be made more efficient by appropriately calibrating them across company lifecycles. Rather than additional early stage funding, innovators in our sample are looking for support to grow “from innovation to operations”

Where experience and data don’t match

Beyond specific findings, there's a deeper insight embedded in our results: perceptions can sometimes mislead. Respondents continue to report difficulty accessing capital with minimal improvement in perceptions since 2019, yet objective indicators show sustained growth in available capital from both domestic and foreign sources. This discrepancy may reflect genuine challenges facing certain technologies, sectors, or business models despite improved overall capital access. It could also stem from some founders having unrealistic expectations about fundraising difficulty: even in well-functioning markets, fundraising is, and to some extent should be, hard.

The distinction matters for policy. If you listen only to entrepreneurs' concerns, you might conclude that the state should simply invest in more companies to ease the fundraising process, a view we do not share. But if you dismiss complaints based on macro statistics showing capital growth, you miss real frictions for some founders or sectors. A complete picture requires both: understanding what entrepreneurs perceive, where those perceptions align with reality, and where and why they diverge.

Where change is possible

Our survey of 300 Icelandic innovators reveals an ecosystem where genuine improvements coexist with persistent structural constraints. While some of them are inherent to Iceland’s context (small market size, geographic isolation) or involve complex policy trade-offs (national currency, tax levels), our survey also identified specific, actionable opportunities for improvement.

Systematically addressing skills gaps through education policy.

Streamlining administrative processes for foreign experts.

Making payment services innovation easier.

Educating foreign investors about Iceland's regulatory environment.

These require coordination across the government and the private sector, but they are well within reach. Acting on them could help sustain Icelandic innovators’ optimism while longer-term, system-level changes take shape.

The article was originally published in Icelandic in Vísbending.

References

- Northstack (2025, desember). Nýsköpunarlandið Ísland 2025.

- European Innovation Scoreboard 2025: Country profile Iceland

- WIPO Global Innovation Index 2025: Iceland Economy Profile

- Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2025: Press release